STRICTLY CONFIDENTIAL Project Kona Fairness opinion analysis February 26,

2026 Exhibit (c)(xii)

STRICTLY CONFIDENTIAL Disclaimer 1. Section name This presentation was prepared

by Rothschild & Co US Inc. (“Rothschild & Co”) on a confidential basis for the benefit and internal use of the Special Committee (the “Special Committee”) of the Board of Directors of KORE Group Holdings, Inc. (the “Company” or “Kona”)

in the context of the Special Committee’s consideration of the matters described herein. In creating this presentation, Rothschild & Co has relied upon information that is publicly available or which was provided to Rothschild & Co by

or on behalf of the Company’s management, including, without limitation, management operating and financial forecasts or projections. Such information involves numerous significant assumptions and subjective determinations that may or may not

be correct. Rothschild & Co has not assumed any responsibility for independent verification of any of such information contained herein, including, but not limited to, any forecasts or projections set forth herein, and Rothschild & Co

has relied on such information being complete and accurate in all material respects. Accordingly, no representation or warranty, express or implied, can be made or is made by Rothschild & Co as to the accuracy or completeness of any such

information or the achievability of any such forecasts or projections. Except where otherwise indicated, this presentation speaks as of the date hereof and is necessarily based upon the information available to Rothschild & Co and

financial, stock market and other conditions and circumstances existing and disclosed to Rothschild & Co as of the date hereof, all of which are subject to change. Rothschild & Co does not have any obligation to update, bring-down,

review or reaffirm this presentation. Under no circumstances should the delivery of this presentation imply that any information or analyses included in this presentation would be the same if made as of any other date. Nothing contained in this

presentation is, or shall be relied upon as, a promise or representation as to the past, present or future. Nothing contained herein shall be deemed to be a recommendation from Rothschild & Co to any party, including without limitation,

any security holder of the Company, to enter into any transaction or to take any course of action. By accepting these materials, the Special Committee acknowledges that Rothschild & Co is not in the business of providing (and the Special

Committee is not relying on Rothschild & Co for) legal, tax or accounting advice, and the Special Committee should receive (and rely on) separate and qualified legal, tax and accounting advice. These materials do not constitute an offer or

solicitation to sell or purchase any securities. Rothschild & Co is not acting in any capacity as a fiduciary or agent of the Special Committee, the Board of Directors of the Company, the Company or the Company’s security holders. In the

ordinary course of their asset management, merchant banking and other business activities, affiliates of Rothschild & Co may at any time hold long or short positions, and may trade or otherwise effect transactions, for their own accounts or

the accounts of their clients in equity, debt or other securities (or related derivative securities) or financial instruments of the Company or any of its affiliates or any other company that may be involved in any transaction. This

presentation is confidential and was not prepared with a view to public disclosure or filing thereof under state or federal securities laws or otherwise. This presentation may not be copied by, or disclosed or made available to, any person

without the prior written consent of Rothschild & Co. This presentation was not prepared for use by readers not as familiar with the business and affairs of the Company as the Special Committee, and accordingly, Rothschild & Co does

not take any responsibility for the accuracy or completeness of any material if used by persons other than the Special Committee. 2

STRICTLY CONFIDENTIAL Contents Executive summary Overview of Standalone

LTP Valuation perspectives Appendix – Valuation supplement 4 10 13 16

1 Executive summary

STRICTLY CONFIDENTIAL Rothschild & Co engagement 5 Rothschild & Co US

Inc. (“Rothschild & Co” or “We”) has been engaged by the Special Committee (the “Special Committee”) of the Board of Directors of Kona (the “Company”) as financial advisor in connection with advising the Special Committee with respect to a

potential transaction (the “Transaction”) proposed by Samoa (together with its affiliated investment funds) and Amelia (collectively, with Samoa, referred herein as the “Samoa Group”) as well as in evaluating potential strategic alternatives to

the Transaction, and if requested by the Special Committee, rendering an opinion to the Special Committee as to the fairness, from a financial point of view, to the Disinterested Stockholders (as defined in the Draft Merger Agreement, dated

February 26, 2026 (the “Agreement”)) of the consideration payable to the Disinterested Stockholders in the Transaction. To this end, these materials focus on the following: Review of Kona’s Standalone LTP (as defined below) Valuation

analysis of Kona In connection with our engagement, Rothschild & Co has, among other things: At the direction of the Special Committee, utilized financial forecasts for Kona, prepared and provided by Kona’s management team (“Management”)

and confirmed and approved for Rothschild & Co’s use by Management and by the Special Committee on February 19, 2026 (the “Standalone Long Term Plan” or “Standalone LTP”) Held discussions with the Special Committee regarding: The

Transaction; Past and current business operations and financial condition and prospects of Kona, including the Standalone LTP and the financial implications thereof; Strategic alternatives available to the Company; and Certain other matters

believed necessary or appropriate to our inquiry Held discussions with key members of Management on a regular basis over the course of our engagement 1.1SITEUxAeTcIOuNtiOvVeEsRuVmIEmWary

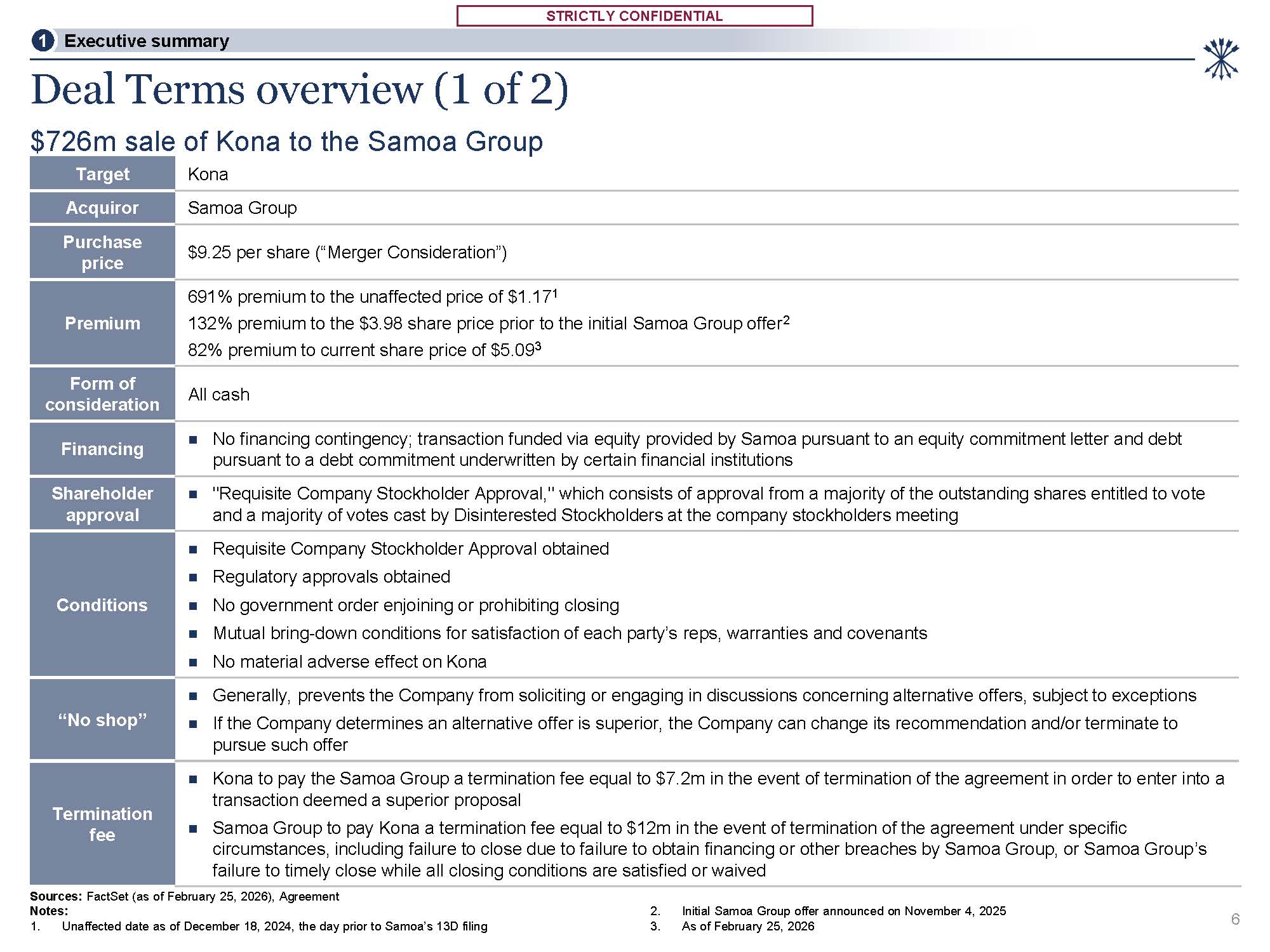

STRICTLY CONFIDENTIAL STRICTLY CONFIDENTIAL Deal Terms overview (1 of

2) 6 Sources: FactSet (as of February 25, 2026), Agreement Notes: 1. Unaffected date as of December 18, 2024, the day prior to Samoa’s 13D filing Initial Samoa Group offer announced on November 4, 2025 As of February 25, 2026 $726m sale

of Kona to the Samoa Group 1 Executive summary Target Kona Acquiror Samoa Group Purchase price $9.25 per share (“Merger Consideration”) Premium 691% premium to the unaffected price of $1.171 132% premium to the $3.98 share price prior

to the initial Samoa Group offer2 82% premium to current share price of $5.093 Form of consideration All cash Financing No financing contingency; transaction funded via equity provided by Samoa pursuant to an equity commitment letter and

debt pursuant to a debt commitment underwritten by certain financial institutions Shareholder approval "Requisite Company Stockholder Approval," which consists of approval from a majority of the outstanding shares entitled to vote and a

majority of votes cast by Disinterested Stockholders at the company stockholders meeting Conditions Requisite Company Stockholder Approval obtained Regulatory approvals obtained No government order enjoining or prohibiting closing Mutual

bring-down conditions for satisfaction of each party’s reps, warranties and covenants No material adverse effect on Kona “No shop” Generally, prevents the Company from soliciting or engaging in discussions concerning alternative offers,

subject to exceptions If the Company determines an alternative offer is superior, the Company can change its recommendation and/or terminate to pursue such offer Termination fee Kona to pay the Samoa Group a termination fee equal to $7.2m

in the event of termination of the agreement in order to enter into a transaction deemed a superior proposal Samoa Group to pay Kona a termination fee equal to $12m in the event of termination of the agreement under specific circumstances,

including failure to close due to failure to obtain financing or other breaches by Samoa Group, or Samoa Group’s failure to timely close while all closing conditions are satisfied or waived

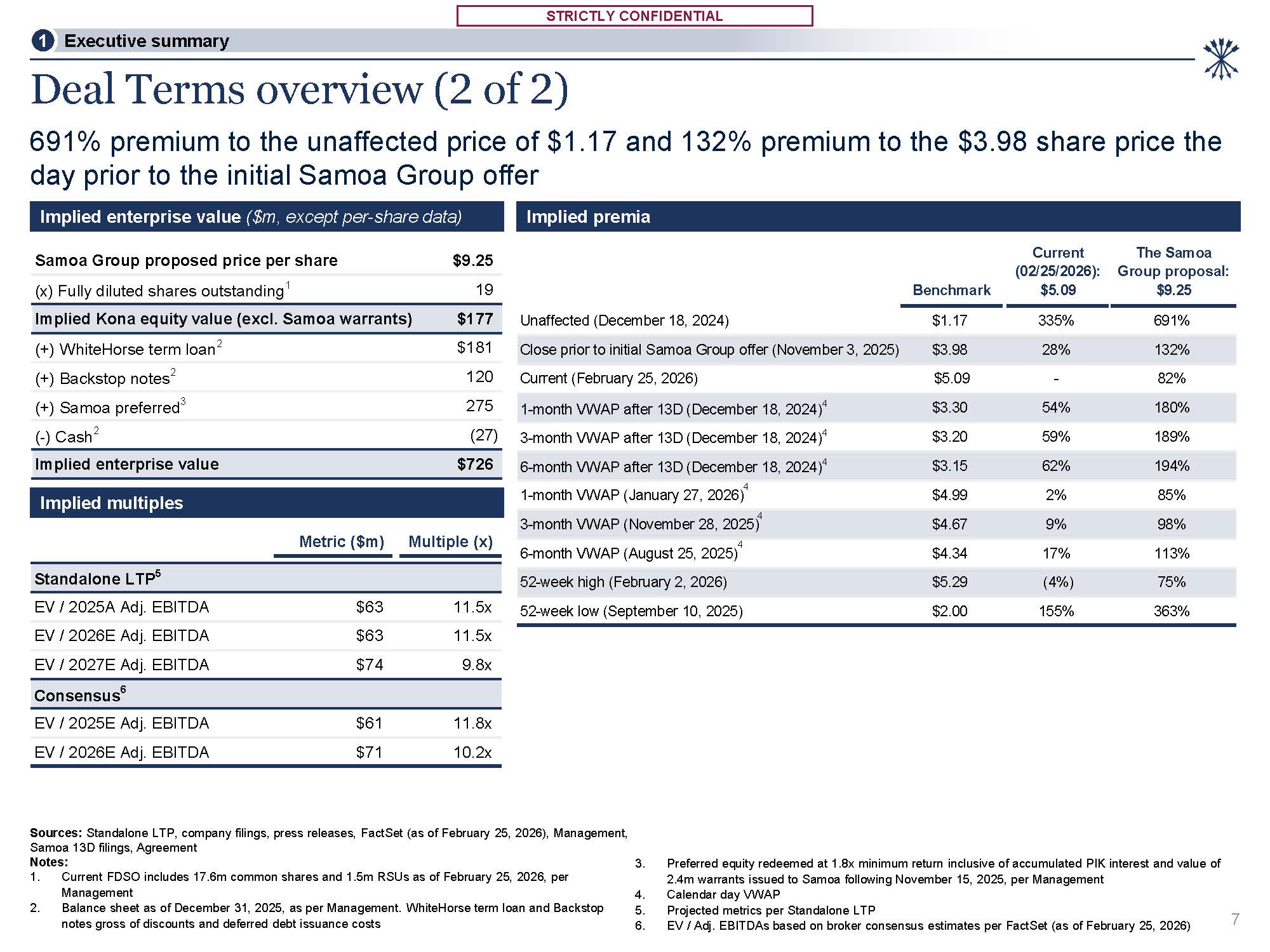

STRICTLY CONFIDENTIAL 4 6-month VWAP (August 25,

2025) $4.34 17% 113% 52-week high (February 2, 2026) $5.29 (4%) 75% 52-week low (September 10, 2025) $2.00 155% 363% Sources: Standalone LTP, company filings, press releases, FactSet (as of February 25, 2026), Management, Samoa 13D

filings, Agreement Notes: Current FDSO includes 17.6m common shares and 1.5m RSUs as of February 25, 2026, per Management Balance sheet as of December 31, 2025, as per Management. WhiteHorse term loan and Backstop notes gross of discounts

and deferred debt issuance costs 3. Preferred equity redeemed at 1.8x minimum return inclusive of accumulated PIK interest and value of 2.4m warrants issued to Samoa following November 15, 2025, per Management Calendar day VWAP Projected

metrics per Standalone LTP EV / Adj. EBITDAs based on broker consensus estimates per FactSet (as of February 25, 2026) Deal Terms overview (2 of 2) Implied enterprise value ($m, except per-share data) Implied premia 7 1 Executive

summary 691% premium to the unaffected price of $1.17 and 132% premium to the $3.98 share price the day prior to the initial Samoa Group offer Implied multiples Metric ($m) Multiple (x) Standalone LTP5 EV / 2025A Adj.

EBITDA $63 11.5x EV / 2026E Adj. EBITDA $63 11.5x EV / 2027E Adj. EBITDA $74 9.8x Consensus6 EV / 2025E Adj. EBITDA $61 11.8x EV / 2026E Adj. EBITDA $71 10.2x 4 1-month VWAP (January 27, 2026) $4.99 2% 85% 4 3-month VWAP

(November 28, 2025) $4.67 9% 98% Samoa Group proposed price per share $9.25 Current (02/25/2026): The Samoa Group proposal: (x) Fully diluted shares outstanding1 19 Benchmark $5.09 $9.25 Implied Kona equity value (excl. Samoa

warrants) $177 Unaffected (December 18, 2024) $1.17 335% 691% (+) WhiteHorse term loan2 $181 Close prior to initial Samoa Group offer (November 3, 2025) $3.98 28% 132% (+) Backstop notes2 120 Current (February 25,

2026) $5.09 - 82% (+) Samoa preferred3 275 1-month VWAP after 13D (December 18, 2024)4 $3.30 54% 180% (-) Cash2 (27) 3-month VWAP after 13D (December 18, 2024)4 $3.20 59% 189% Implied enterprise value $726 6-month VWAP after

13D (December 18, 2024)4 $3.15 62% 194%

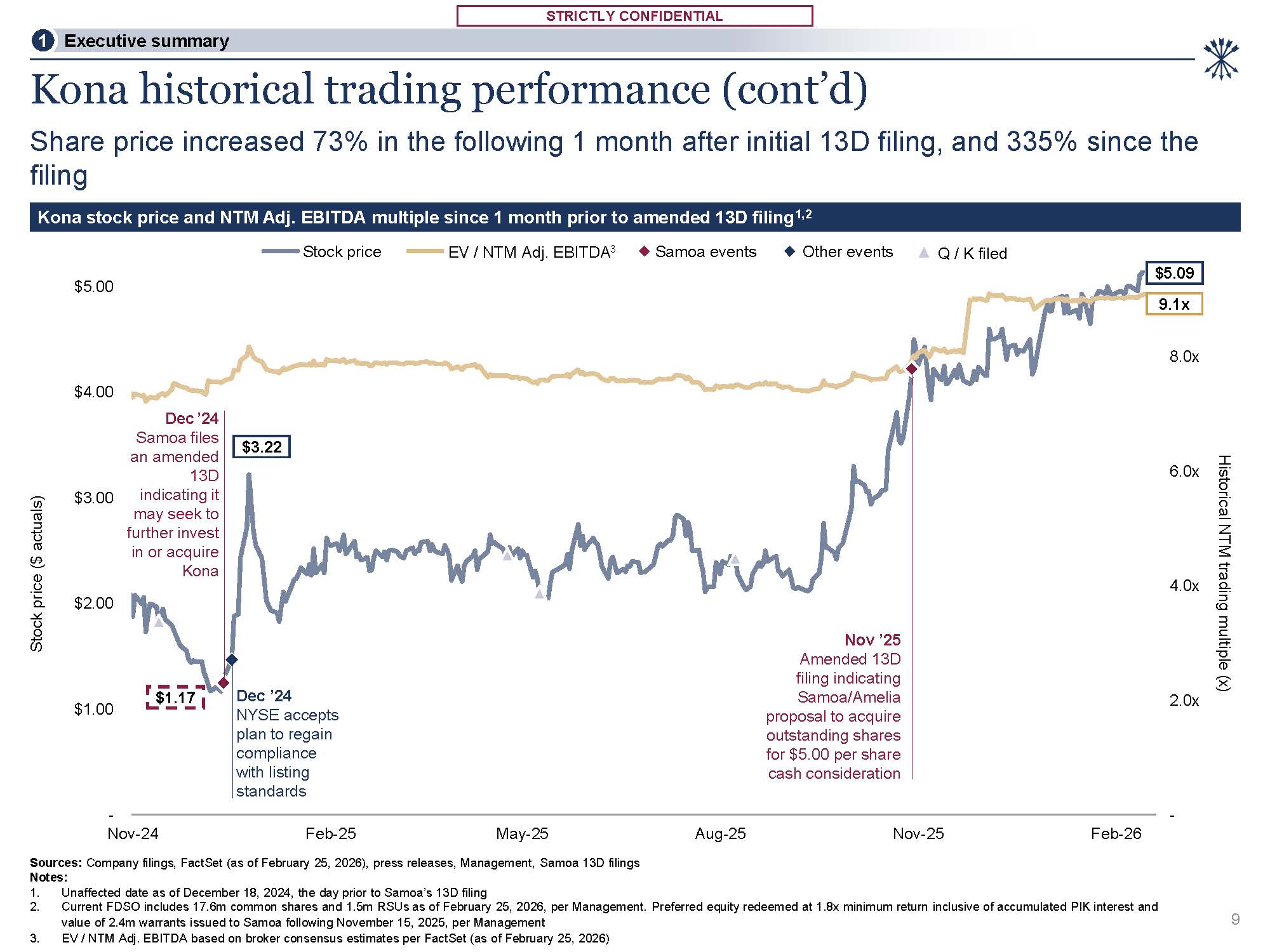

STRICTLY CONFIDENTIAL STRICTLY CONFIDENTIAL Dec ’24 Samoa files an amended 13D

indicating it may seek to further invest in or acquire Kona - 2.0x 4.0x 6.0x 8.0x 10.0x 12.0x 14.0x 16.0x $5.00 $10.00 $15.00 $20.00 $25.00 $30.00 $35.00 $40.00 $45.00 $50.00 Jan-26 Dec ’24 NYSE accepts plan to regain

compliance with listing standards 1 Executive summary Mar ’23 Announces acquisition of Twilio’s IoT business unit Jun ’24 1:5 reverse stock split Nov ’24 Completes operational restructuring plan Nov ’23 Kona reports strategic

investment from Samoa disclosing 12.0% ownership3 Apr ’24 CEO transition Feb ’22 Announces acquisition of Business Mobility Partners & SIMON Kona historical trading performance Merger Consideration represents a 691% premium to the

unaffected price of $1.17 and 132% premium to the $3.98 share price prior to the initial Samoa Group offer Sources: Company filings, FactSet (as of February 25, 2026), press releases, Samoa 13D filings, Agreement Notes: Current FDSO

includes 17.6m common shares and 1.5m RSUs as of February 25, 2026, per Management. Preferred equity redeemed at 1.8x minimum return inclusive of accumulated PIK interest and value of 2.4m warrants issued to Samoa following November 15, 2025,

per Management EV / NTM Adj. EBITDA based on broker consensus estimates per FactSet (as of February 25, 2026) Ownership percentage calculated including the 2.4m warrants issued to Samoa, per Management Kona stock price and NTM Adj. EBITDA

multiple since 2021 de-SPAC1 Stock price ($ actuals) Historical NTM trading multiple (x) Stock price EV / NTM Adj. EBITDA2 Samoa events Other events Q / K filed $5.09 9.1x Nov ’25 Amended 13D filing indicating Samoa / Amelia proposal

to acquire outstanding shares for $5.00 per share cash consideration - Sep-21 Jan-22 May-22 Sep-22 Jan-23 May-23 Sep-23 Jan-24 May-24 Sep-24 Jan-25 May-25 Sep-25 Feb-26 8

STRICTLY CONFIDENTIAL STRICTLY CONFIDENTIAL - 2.0x 4.0x 6.0x 8.0x - Nov-24

Feb-25 May-25 Sources: Company filings, FactSet (as of February 25, 2026), press releases, Management, Samoa 13D filings Notes: $1.00 $2.00 $3.00 $4.00 $5.00 Aug-25 Nov-25 Feb-26 Kona historical trading performance (cont’d) Share

price increased 73% in the following 1 month after initial 13D filing, and 335% since the filing Kona stock price and NTM Adj. EBITDA multiple since 1 month prior to amended 13D filing1,2 9.1x $1.17 $5.09 $3.22 Dec ’24 Samoa files an

amended 13D indicating it may seek to further invest in or acquire Kona Historical NTM trading multiple (x) Dec ’24 NYSE accepts plan to regain compliance with listing standards Unaffected date as of December 18, 2024, the day prior to

Samoa’s 13D filing Current FDSO includes 17.6m common shares and 1.5m RSUs as of February 25, 2026, per Management. Preferred equity redeemed at 1.8x minimum return inclusive of accumulated PIK interest and value of 2.4m warrants issued to

Samoa following November 15, 2025, per Management EV / NTM Adj. EBITDA based on broker consensus estimates per FactSet (as of February 25, 2026) Nov ’25 Amended 13D filing indicating Samoa/Amelia proposal to acquire outstanding shares for

$5.00 per share cash consideration 9 1 Executive summary Stock price ($ actuals) Stock price EV / NTM Adj. EBITDA3 Samoa events Other events Q / K filed

2 Overview of Standalone LTP

STRICTLY CONFIDENTIAL STRICTLY

CONFIDENTIAL 8.5% 8.9% 10.2% 12.0% 12.1% 19.8 21.5 23.7 26.6 29.8 2025A 2026E 2027E 2028E Sources: Management, Standalone LTP Note: 2029E 2bps (4bps) 31bps 22bps 11bps 56.3% 56.3%

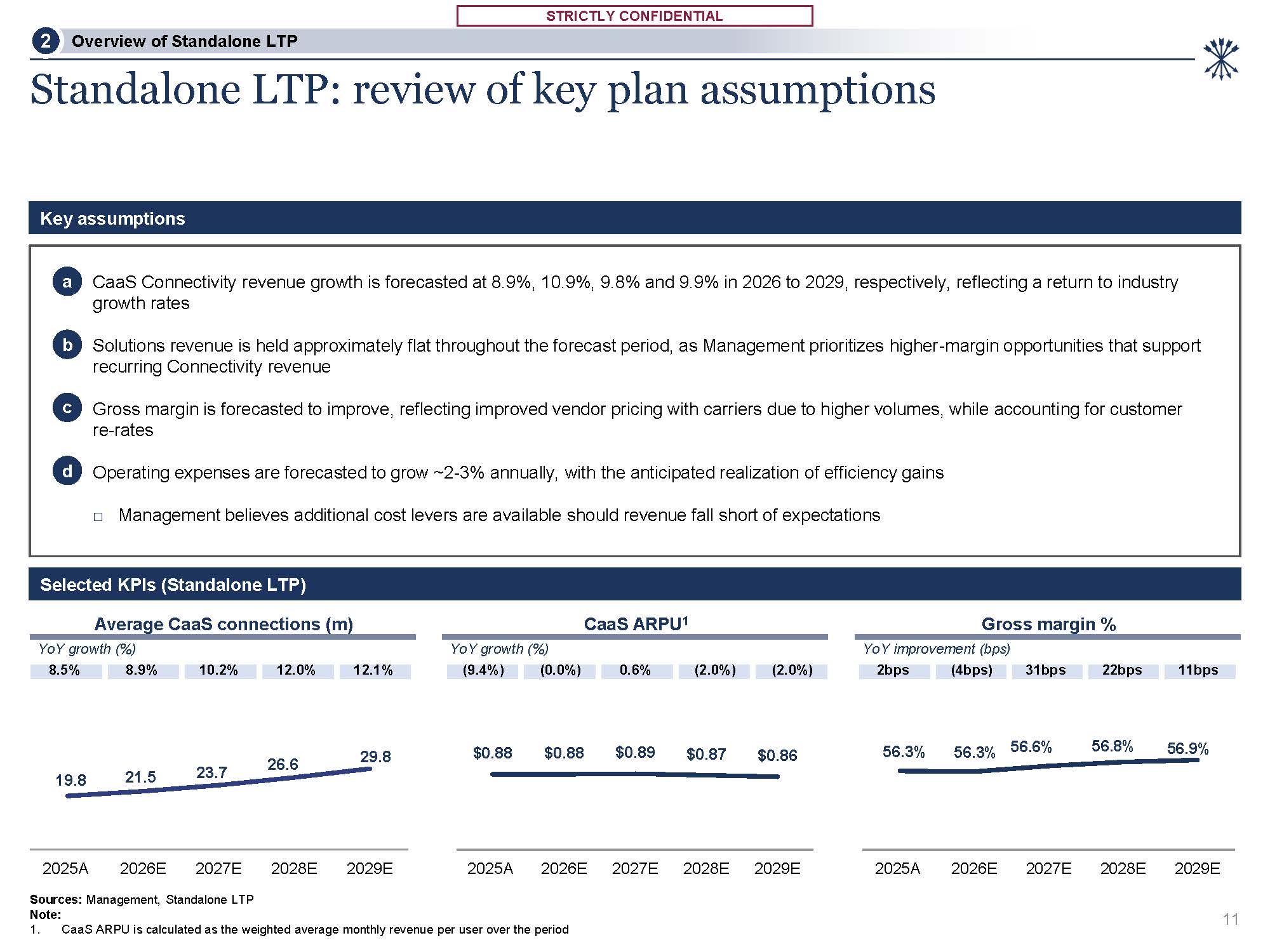

56.6% 56.8% 56.9% 2025A 2026E 2027E 2028E 2029E (9.4%) (0.0%) 0.6% (2.0%) (2.0%) $0.88 $0.88 $0.89 $0.87 $0.86 2025A 2026E 2027E 2028E 2029E Standalone LTP: review of key plan assumptions 1. CaaS ARPU is calculated as

the weighted average monthly revenue per user over the period Selected KPIs (Standalone LTP) Key assumptions a CaaS Connectivity revenue growth is forecasted at 8.9%, 10.9%, 9.8% and 9.9% in 2026 to 2029, respectively, reflecting a return

to industry growth rates b Solutions revenue is held approximately flat throughout the forecast period, as Management prioritizes higher-margin opportunities that support recurring Connectivity revenue c Gross margin is forecasted to

improve, reflecting improved vendor pricing with carriers due to higher volumes, while accounting for customer re-rates d Operating expenses are forecasted to grow ~2-3% annually, with the anticipated realization of efficiency

gains Management believes additional cost levers are available should revenue fall short of expectations Average CaaS connections (m) CaaS ARPU1 Gross margin % YoY growth (%) YoY growth (%) YoY improvement (bps) Overview of Standalone

LTP 2 11

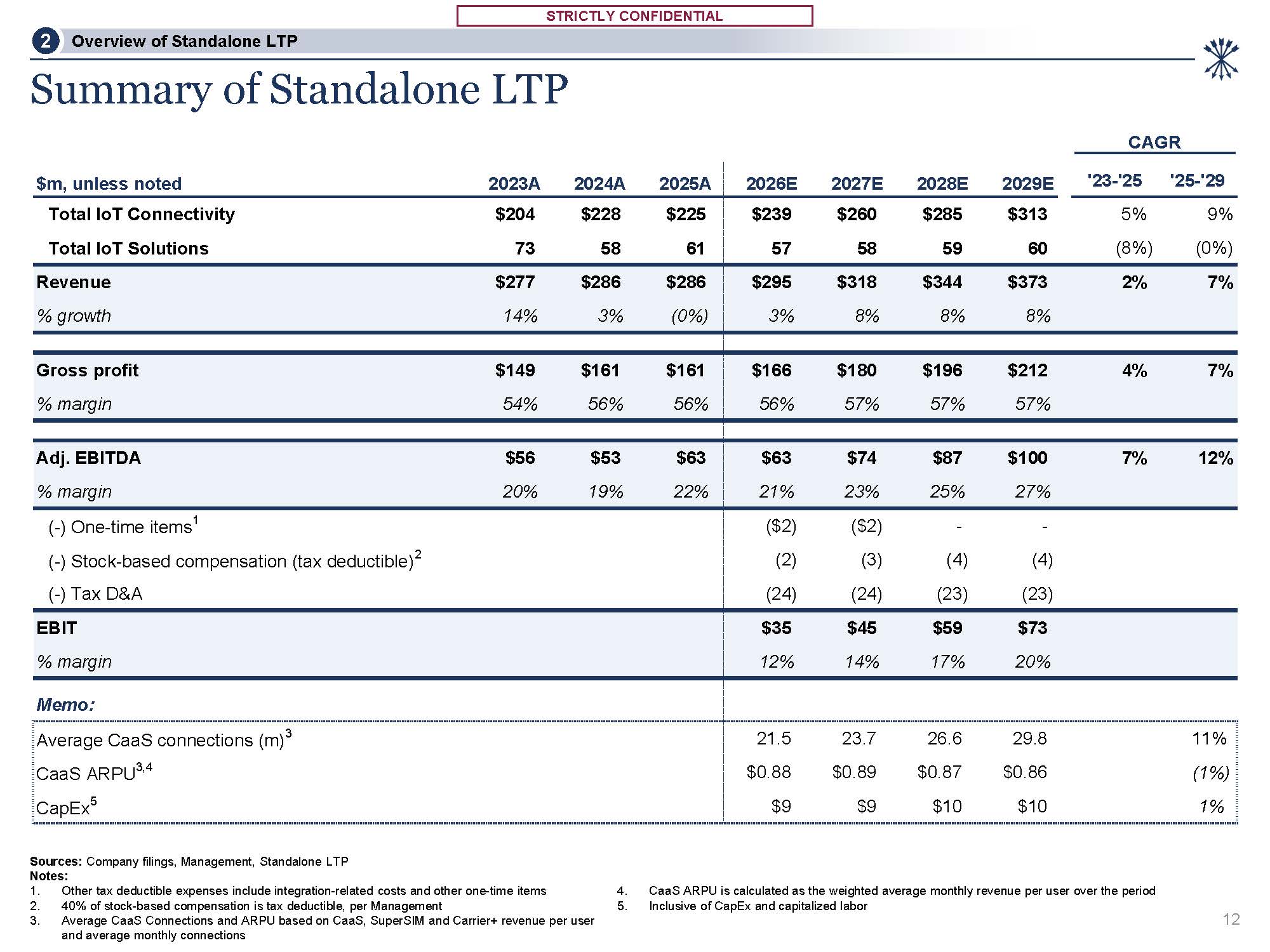

STRICTLY CONFIDENTIAL STRICTLY CONFIDENTIAL CAGR $m, unless noted 2023A 2024A

2025A 2026E 2027E 2028E 2029E '23-'25 '25-'29 Total IoT Connectivity $204 $228 $225 Total IoT Solutions 73 58 61 $239 $260 $285 $313 57 58 59 60 5% 9% (8%) (0%) Revenue $277 $286 $286 % growth 14% 3% (0%) $295 $318 $344 $373 2%

7% 3% 8% 8% 8% Gross profit $149 $161 $161 % margin 54% 56% 56% $166 $180 $196 $212 4% 7% 56% 57% 57% 57% Adj. EBITDA $56 $53 $63 % margin 20% 19% 22% $63 $74 $87 $100 7% 12% 21% 23% 25% 27% (-) One-time items1 (-) Stock-based

compensation (tax deductible)2 (-) Tax D&A ($2) ($2) - - (2) (3) (4) (4) (24) (24) (23) (23) EBIT % margin $35 $45 $59 $73 12% 14% 17% 20% Memo: Average CaaS connections (m)3 CaaS ARPU3,4 CapEx5 21.5 23.7 26.6 29.8 11% $0.88

$0.89 $0.87 $0.86 (1%) $9 $9 $10 $10 1% Summary of Standalone LTP Sources: Company filings, Management, Standalone LTP Notes: Other tax deductible expenses include integration-related costs and other one-time items 40% of stock-based

compensation is tax deductible, per Management Average CaaS Connections and ARPU based on CaaS, SuperSIM and Carrier+ revenue per user and average monthly connections CaaS ARPU is calculated as the weighted average monthly revenue per user

over the period Inclusive of CapEx and capitalized labor 12 Overview of Standalone LTP 2

3 Valuation perspectives

STRICTLY CONFIDENTIAL STRICTLY CONFIDENTIAL Overview of valuation methodologies

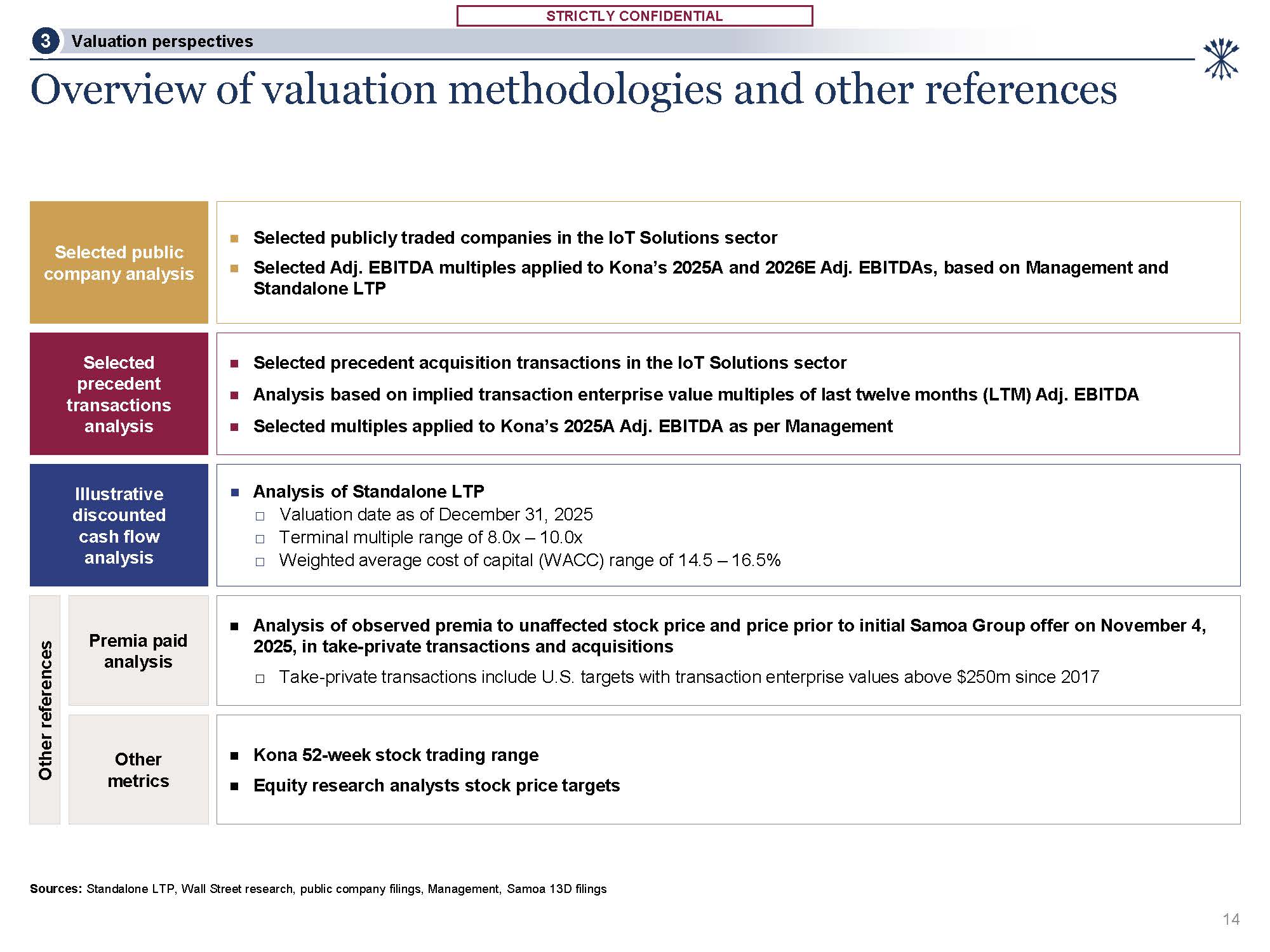

and other references Selected public company analysis Selected publicly traded companies in the IoT Solutions sector Selected Adj. EBITDA multiples applied to Kona’s 2025A and 2026E Adj. EBITDAs, based on Management and Standalone

LTP Selected precedent acquisition transactions in the IoT Solutions sector Analysis based on implied transaction enterprise value multiples of last twelve months (LTM) Adj. EBITDA Selected multiples applied to Kona’s 2025A Adj. EBITDA as

per Management Selected precedent transactions analysis Analysis of Standalone LTP Valuation date as of December 31, 2025 Terminal multiple range of 8.0x – 10.0x Weighted average cost of capital (WACC) range of 14.5 – 16.5% Illustrative

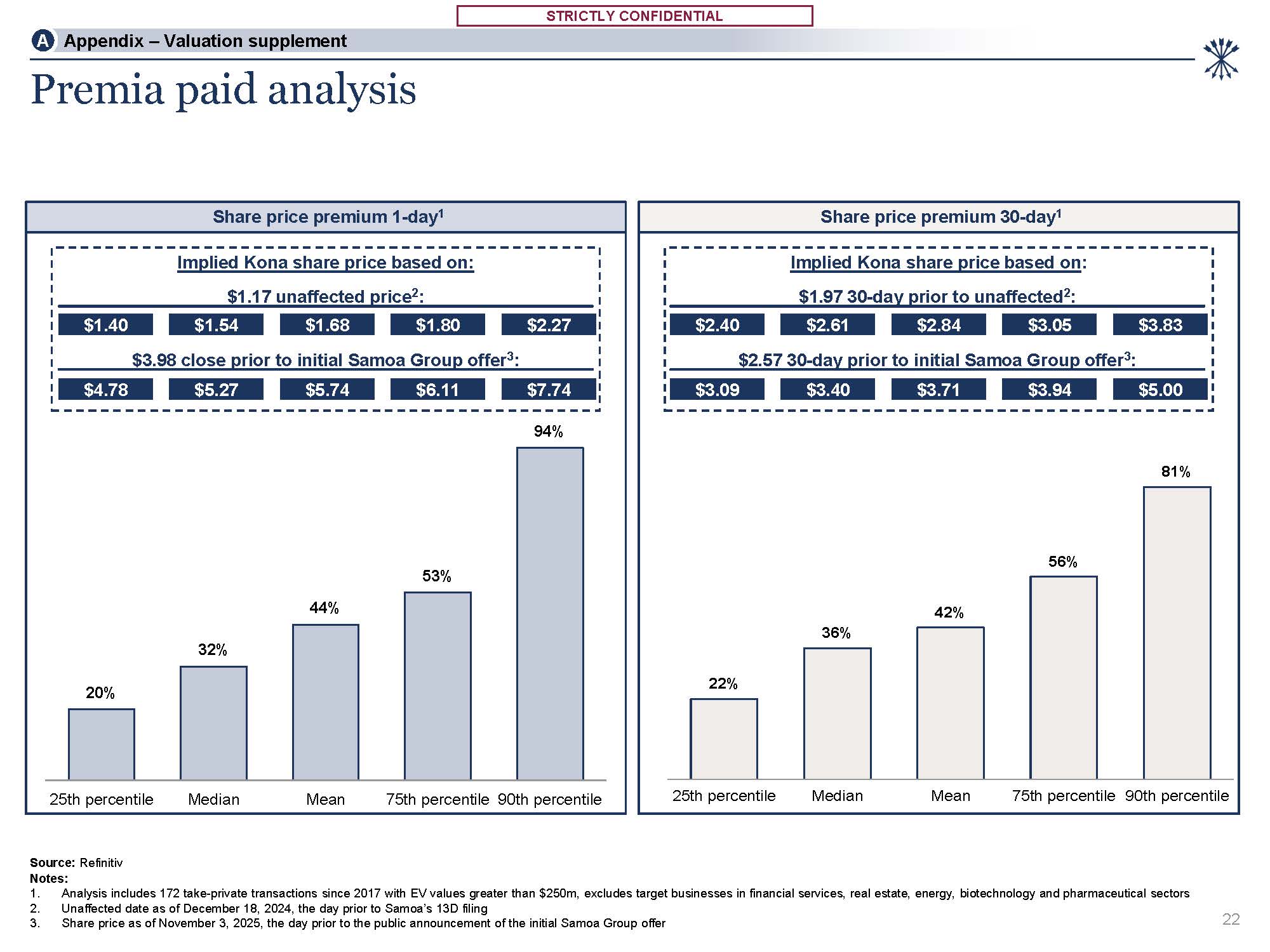

discounted cash flow analysis Other references Premia paid analysis Analysis of observed premia to unaffected stock price and price prior to initial Samoa Group offer on November 4, 2025, in take-private transactions and acquisitions □

Take-private transactions include U.S. targets with transaction enterprise values above $250m since 2017 Other metrics Kona 52-week stock trading range Equity research analysts stock price targets 14 Sources: Standalone LTP, Wall Street

research, public company filings, Management, Samoa 13D filings Valuation perspectives 3

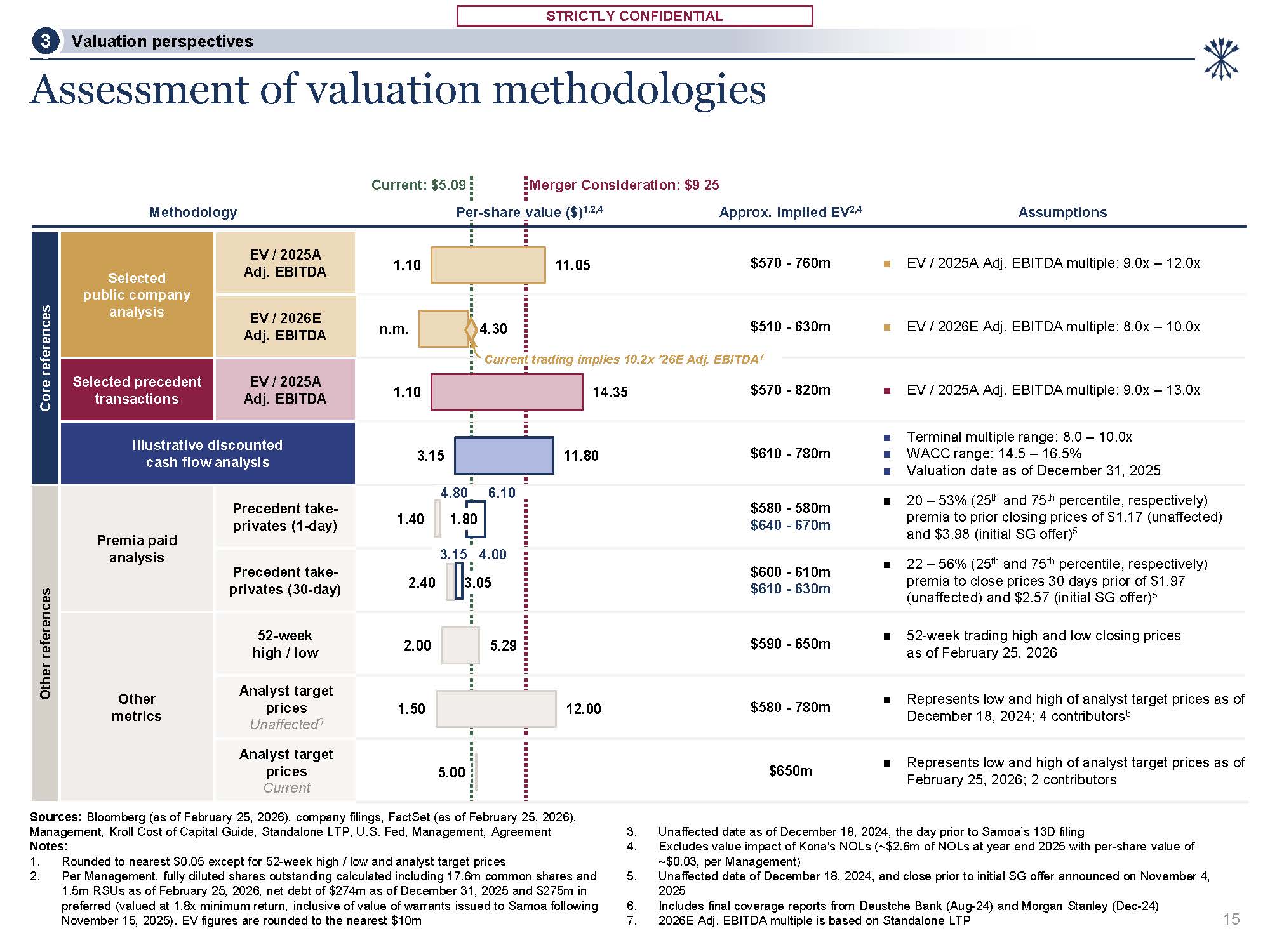

STRICTLY CONFIDENTIAL STRICTLY CONFIDENTIAL Methodology Current: $5.09 Merger

Consideration: $9.25 Per-share value ($)1,2,4 Approx. implied EV2,4 Assumptions Core references Selected public company analysis EV / 2025A Adj. EBITDA $570 - 760m EV / 2025A Adj. EBITDA multiple: 9.0x – 12.0x EV / 2026E Adj.

EBITDA $510 - 630m EV / 2026E Adj. EBITDA multiple: 8.0x – 10.0x Selected precedent transactions EV / 2025A Adj. EBITDA Illustrative discounted cash flow analysis Other references Premia paid analysis Precedent take- privates

(1-day) $580 - 580m $640 - 670m 20 – 53% (25th and 75th percentile, respectively) premia to prior closing prices of $1.17 (unaffected) and $3.98 (initial SG offer)5 Precedent take-privates (30-day) $600 - 610m $610 - 630m 22 – 56% (25th

and 75th percentile, respectively) premia to close prices 30 days prior of $1.97 (unaffected) and $2.57 (initial SG offer)5 Other metrics 52-week high / low $590 - 650m 52-week trading high and low closing prices as of February 25,

2026 Analyst target prices Unaffected3 $580 - 780m Represents low and high of analyst target prices as of December 18, 2024; 4 contributors6 Analyst target prices Current $650m Represents low and high of analyst target prices as of

February 25, 2026; 2 contributors 1.10 n.m. 2.00 1.50 5.00 11.05 4.30 1.10 14.35 $570 - 820m EV / 2025A Adj. EBITDA multiple: 9.0x – 13.0x Terminal multiple range: 8.0 – 10.0x 3.15 11.80 $610 - 780m WACC range: 14.5 –

16.5% Valuation date as of December 31, 2025 1.40 1.80 2.40 3.05 5.29 12.00 Assessment of valuation methodologies Sources: Bloomberg (as of February 25, 2026), company filings, FactSet (as of February 25, 2026), Management, Kroll Cost of

Capital Guide, Standalone LTP, U.S. Fed, Management, Agreement Notes: Rounded to nearest $0.05 except for 52-week high / low and analyst target prices Per Management, fully diluted shares outstanding calculated including 17.6m common shares

and 1.5m RSUs as of February 25, 2026, net debt of $274m as of December 31, 2025 and $275m in preferred (valued at 1.8x minimum return, inclusive of value of warrants issued to Samoa following November 15, 2025). EV figures are rounded to the

nearest $10m Unaffected date as of December 18, 2024, the day prior to Samoa’s 13D filing Excludes value impact of Kona's NOLs (~$2.6m of NOLs at year end 2025 with per-share value of ~$0.03, per Management) Unaffected date of December 18,

2024, and close prior to initial SG offer announced on November 4, 2025 Includes final coverage reports from Deustche Bank (Aug-24) and Morgan Stanley (Dec-24) 2026E Adj. EBITDA multiple is based on Standalone LTP 15 4.80 6.10 3.15

4.00 Current trading implies 10.2x ’26E Adj. EBITDA7 Valuation perspectives 3

4 Appendix – Valuation supplement

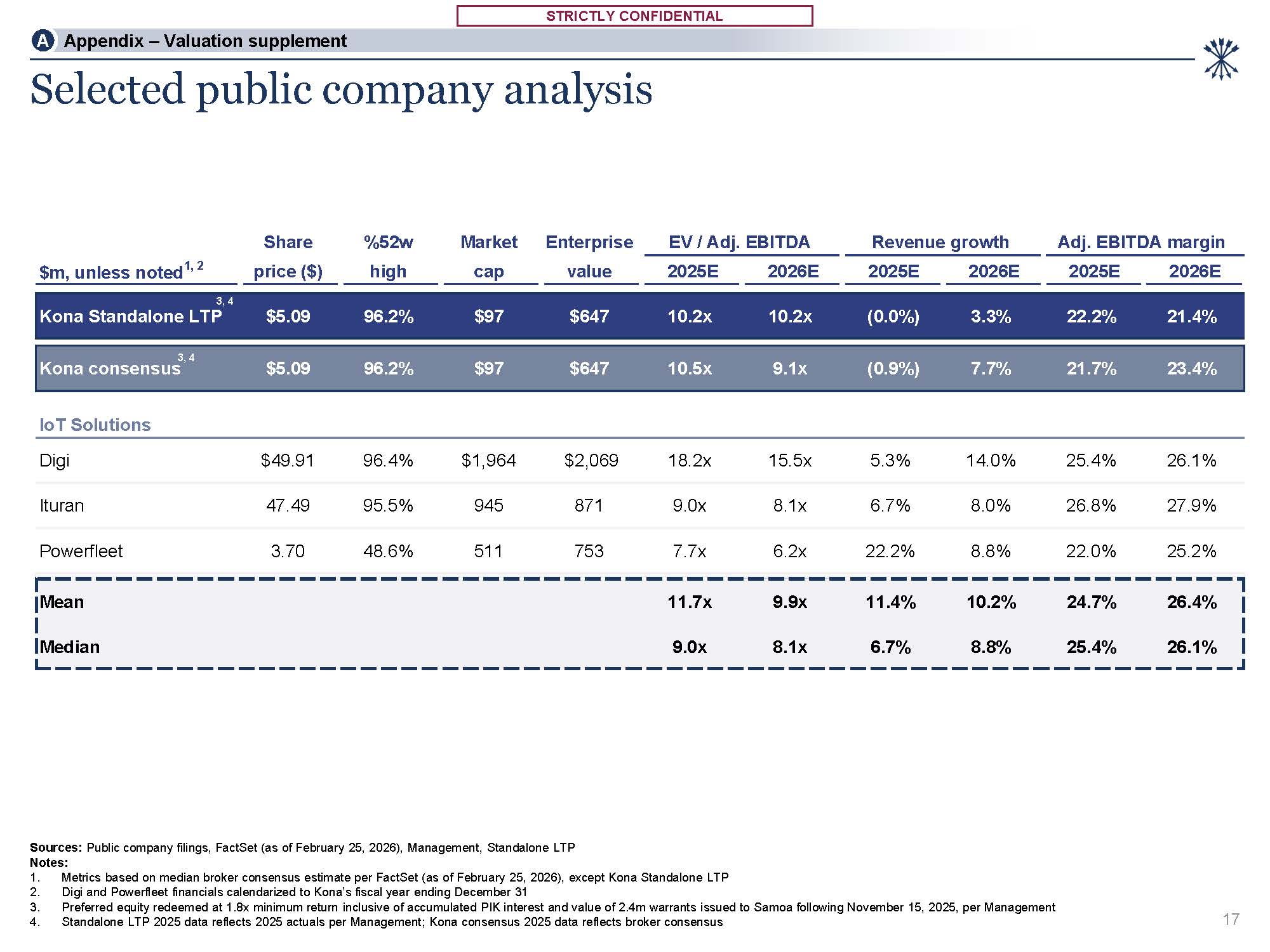

STRICTLY CONFIDENTIAL STRICTLY CONFIDENTIAL 3, 4 Kona Standalone

LTP $5.09 96.2% $97 $647 10.2x 10.2x (0.0%) 3.3% 22.2% 21.4% 3, 4 Kona consensus $5.09 96.2% $97 $647 10.5x 9.1x (0.9%) 7.7% 21.7% 23.4% IoT

Solutions Digi $49.91 96.4% $1,964 $2,069 18.2x 15.5x 5.3% 14.0% 25.4% 26.1% Ituran 47.49 95.5% 945 871 9.0x 8.1x 6.7% 8.0% 26.8% 27.9% Powerfleet 3.70 48.6% 511 753 7.7x 6.2x 22.2% 8.8% 22.0% 25.2% Mean 11.7x 9.9x 11.4% 10.2% 24.7% 26.4% Median 9.0x 8.1x 6.7% 8.8% 25.4% 26.1% Share %52w Market Enterprise EV

/ Adj. EBITDA Revenue growth Adj. EBITDA margin $m, unless noted1, 2 price ($) high cap value 2025E 2026E 2025E 2026E 2025E 2026E Selected public company analysis Sources: Public company filings, FactSet (as of February 25, 2026),

Management, Standalone LTP Notes: Metrics based on median broker consensus estimate per FactSet (as of February 25, 2026), except Kona Standalone LTP Digi and Powerfleet financials calendarized to Kona’s fiscal year ending December

31 Preferred equity redeemed at 1.8x minimum return inclusive of accumulated PIK interest and value of 2.4m warrants issued to Samoa following November 15, 2025, per Management Standalone LTP 2025 data reflects 2025 actuals per Management;

Kona consensus 2025 data reflects broker consensus 17 A Appendix – Valuation supplement

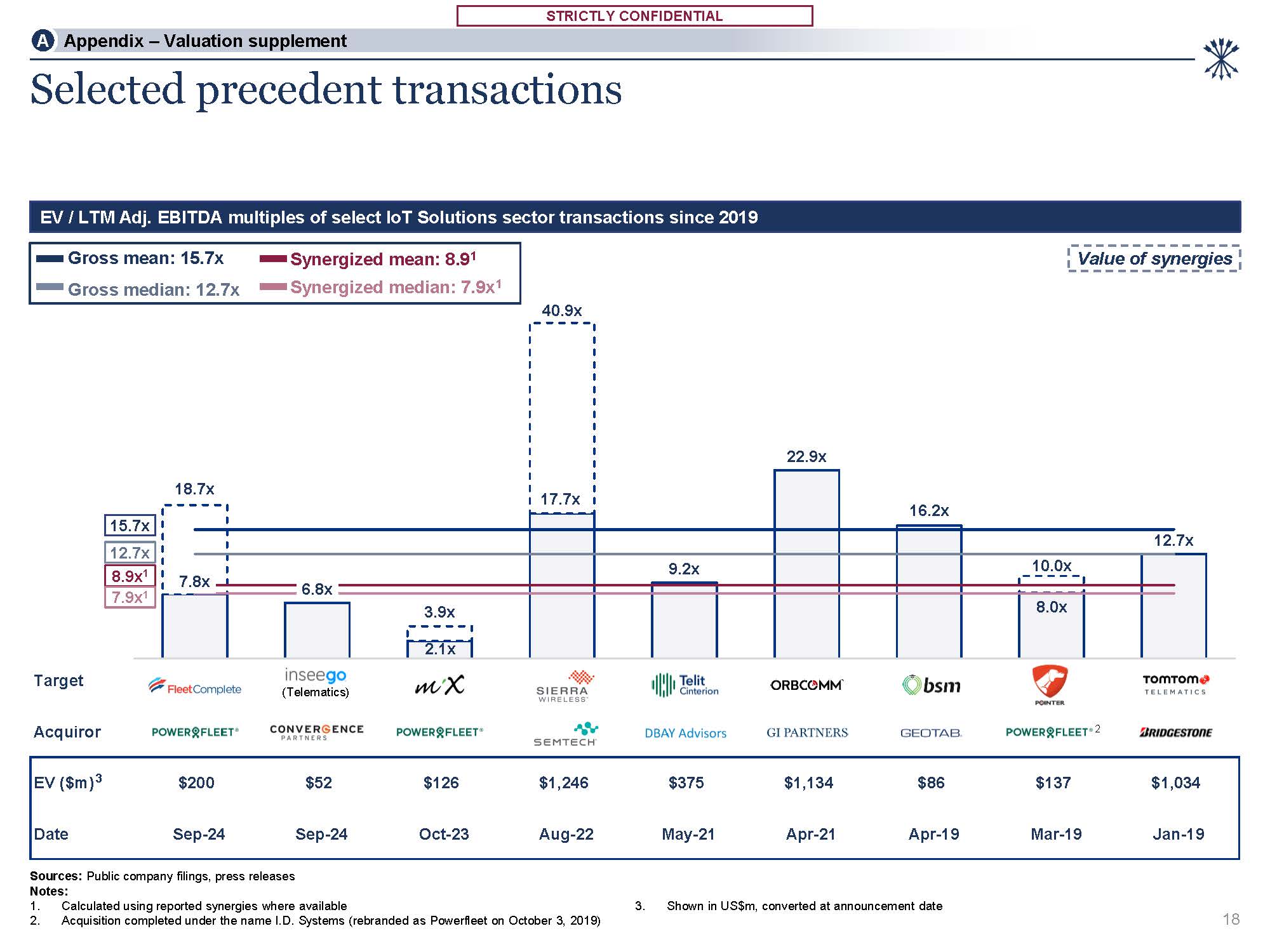

STRICTLY CONFIDENTIAL STRICTLY CONFIDENTIAL A Appendix – Valuation

supplement Target Acquiror EV

($m)3 $200 $52 $126 $1,246 $375 $1,134 $86 $137 $1,034 Date Sep-24 Sep-24 Oct-23 Aug-22 May-21 Apr-21 Apr-19 Mar-19 Jan-19 7.8x 2.1x 17.7x 8.0x 18.7x 6.8x 3.9x 40.9x 9.2x 22.9x 16.2x 10.0x 12.7x Selected

precedent transactions Sources: Public company filings, press releases Notes: Calculated using reported synergies where available Acquisition completed under the name I.D. Systems (rebranded as Powerfleet on October 3, 2019) 3. Shown in

US$m, converted at announcement date EV / LTM Adj. EBITDA multiples of select IoT Solutions sector transactions since 2019 (Telematics) 2 Value of synergies 15.7x 12.7x 8.9x1 7.9x1 Gross mean: 15.7x Gross median: 12.7x Synergized

mean: 8.91 Synergized median: 7.9x1 18

STRICTLY CONFIDENTIAL STRICTLY CONFIDENTIAL A Appendix – Valuation

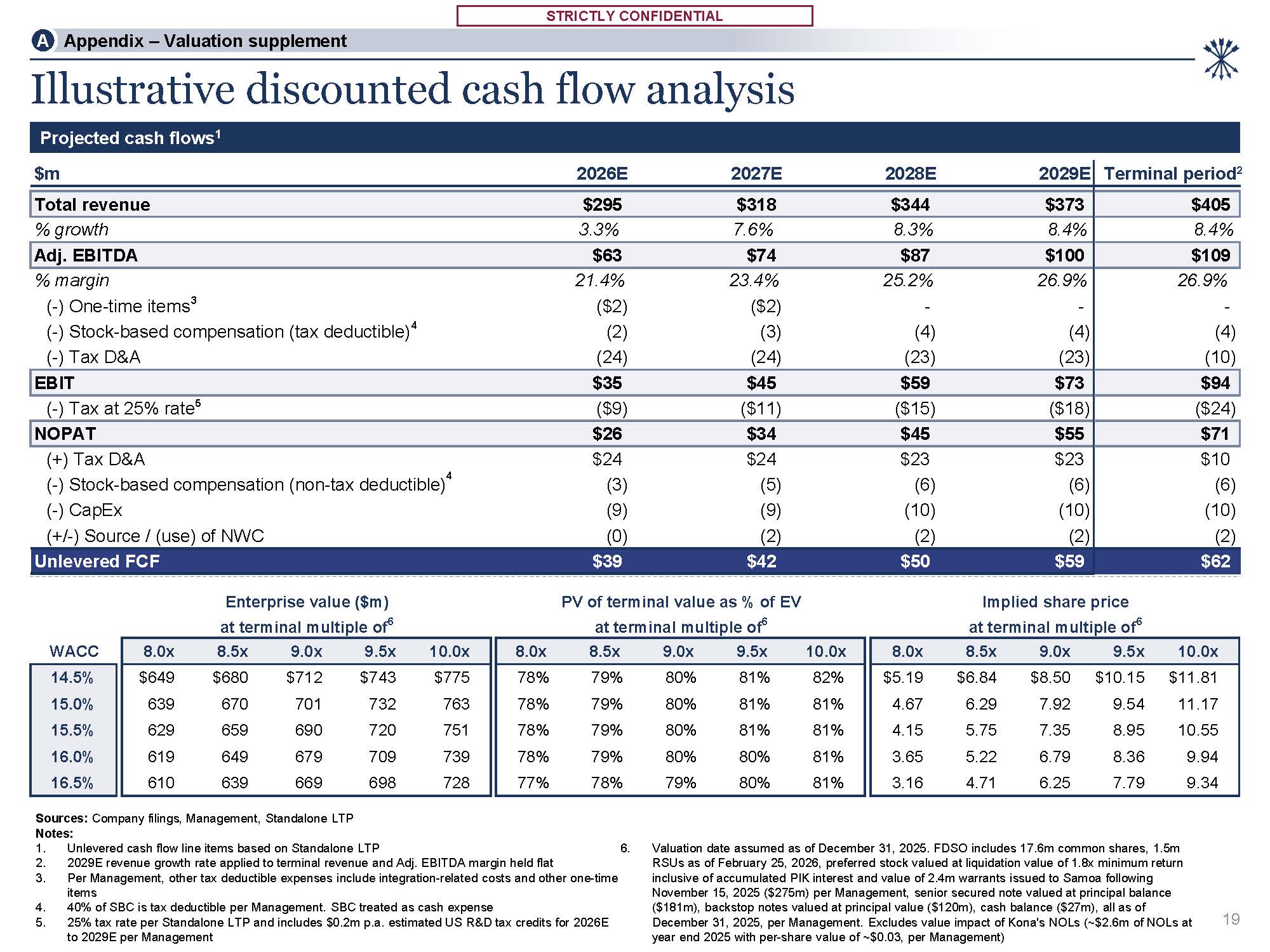

supplement Illustrative discounted cash flow analysis Projected cash flows1 $m 2026E 2027E 2028E 2029E Terminal period2 Total revenue $295 $318 $344 $373 $405 % growth 3.3% 7.6% 8.3% 8.4% 8.4% Adj.

EBITDA $63 $74 $87 $100 $109 % margin 21.4% 23.4% 25.2% 26.9% 26.9% (-) One-time items3 ($2) ($2) - - - (-) Stock-based compensation (tax deductible)4 (2) (3) (4) (4) (4) (-) Tax

D&A (24) (24) (23) (23) (10) EBIT $35 $45 $59 $73 $94 (-) Tax at 25% rate5 ($9) ($11) ($15) ($18) ($24) NOPAT $26 $34 $45 $55 $71 (+) Tax D&A $24 $24 $23 $23 $10 (-) Stock-based compensation (non-tax

deductible)4 (3) (5) (6) (6) (6) (-) CapEx (9) (9) (10) (10) (10) (+/-) Source / (use) of NWC (0) (2) (2) (2) (2) Unlevered FCF $39 $42 $50 $59 $62 Sources: Company filings, Management, Standalone LTP Notes: Unlevered

cash flow line items based on Standalone LTP 2029E revenue growth rate applied to terminal revenue and Adj. EBITDA margin held flat Per Management, other tax deductible expenses include integration-related costs and other one-time items 40%

of SBC is tax deductible per Management. SBC treated as cash expense 25% tax rate per Standalone LTP and includes $0.2m p.a. estimated US R&D tax credits for 2026E to 2029E per Management 6. Valuation date assumed as of December 31, 2025.

FDSO includes 17.6m common shares, 1.5m RSUs as of February 25, 2026, preferred stock valued at liquidation value of 1.8x minimum return inclusive of accumulated PIK interest and value of 2.4m warrants issued to Samoa following November 15,

2025 ($275m) per Management, senior secured note valued at principal balance ($181m), backstop notes valued at principal value ($120m), cash balance ($27m), all as of December 31, 2025, per Management. Excludes value impact of Kona's NOLs

(~$2.6m of NOLs at year end 2025 with per-share value of ~$0.03, per

Management) 19 WACC 8.0x 8.5x 9.0x 9.5x 10.0x 8.0x 8.5x 9.0x 9.5x 10.0x 8.0x 8.5x 9.0x 9.5x 10.0x 14.5% $649 $680 $712 $743 $775 78% 79% 80% 81% 82% $5.19 $6.84 $8.50 $10.15 $11.81 15.0% 639 670 701 732 763 78% 79% 80% 81% 81% 4.67 6.29 7.92 9.54 11.17 15.5% 629 659 690 720 751 78% 79% 80% 81% 81% 4.15 5.75 7.35 8.95 10.55 16.0% 619 649 679 709 739 78% 79% 80% 80% 81% 3.65 5.22 6.79 8.36 9.94 16.5% 610 639 669 698 728 77% 78% 79% 80% 81% 3.16 4.71 6.25 7.79 9.34 Enterprise

value ($m) PV of terminal value as % of EV Implied share price at terminal multiple of6 at terminal multiple of6 at terminal multiple of6

STRICTLY CONFIDENTIAL STRICTLY

CONFIDENTIAL $3.15 $5.08 $6.48 $1.45 $12.88 $10.40 $8.81 $8.42 Illustrative discounted cash flow analysis sensitivity DCF sensitivity to various operating assumptions Item Standalone LTP assumption Sensitivity range Implied per-share

midpoint DCF range1 Sources: Company filings, Management, Standalone LTP Notes: 1. Sensitivity analyses vs. Standalone LTP. Valuation date assumed as of December 31, 2025. FDSO includes 17.6m common shares and 1.5m RSUs as of February 25,

2026, per Management. Preferred equity redeemed at 1.8x minimum return inclusive of accumulated PIK interest and value of 4. 2.4m warrants issued to Samoa following November 15, 2025, per Management. Assumes WACC of 15.5% and terminal

multiple midpoint of 9.0x. Excludes value impact of Kona's NOLs (~$2.6m of NOLs at year end 2025 with per-share value of ~$0.03, per Management) 2025A to 2029E CAGR 56.3% represents 2025A gross margin per Management. 57.9% represents 2029E

Standalone LTP gross margin +1% 21.4% represents 2026E Standalone LTP Adj. EBITDA margin and 27.9% represents 2029E Standalone LTP Adj. EBITDA margin +1% Avg. CaaS connections (% CAGR)2 Average CaaS connections reach 29.8m by

2029 2025–2029 CAGR of 11% 9% 13% 11% Solutions (% CAGR)2 IoT Solutions has (0.3%) CAGR across 2025 to 2029 (5%) 5% (0.3%) Gross margin (% +/-) Gross margin increases from 56.3% in 2025 to 56.9% in 2029 56.3%3 57.9%3 56.9% Adj.

EBITDA margin increases from 22.2% in 2025 to 26.9% in 2029 Terminal Adj. EBITDA margin 21.4%4 27.9%4 26.9% 20 TMM Base DCF midpoint: $7.35 A Appendix – Valuation supplement

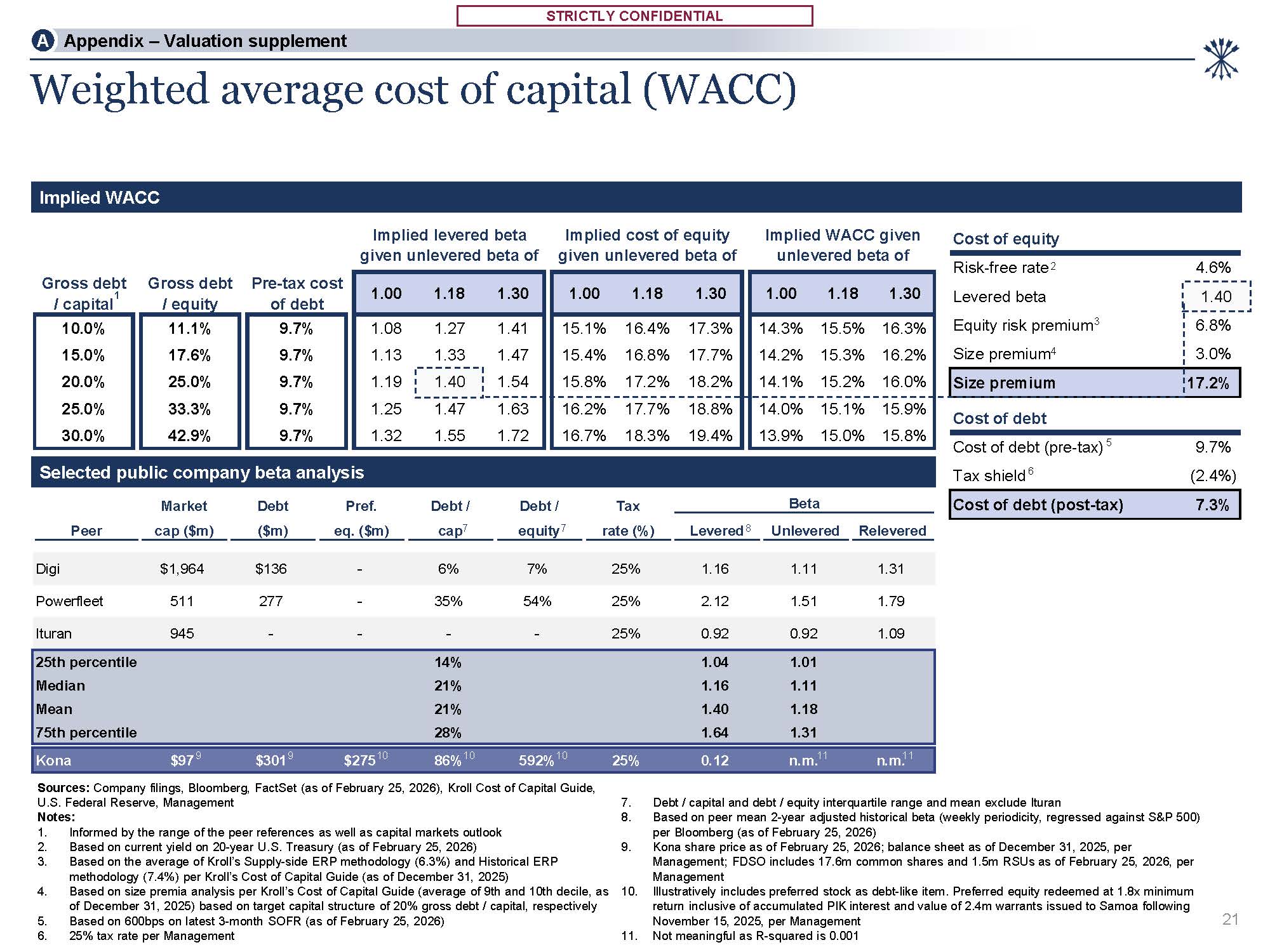

STRICTLY CONFIDENTIAL STRICTLY CONFIDENTIAL Implied levered beta given unlevered

beta of Implied cost of equity given unlevered beta of Implied WACC given unlevered beta of Selected public company beta analysis Tax shield 6 (2.4%) Market Debt Pref. Debt / Debt / Tax Beta Cost of debt (post-tax) 7.3% Peer cap

($m) ($m) eq. ($m) cap7 equity7 rate (%) Levered8 Unlevered Relevered Digi $1,964 $136 - 6% 7% 25% 1.16 1.11 1.31 Powerfleet 511 277 - 35% 54% 25% 2.12 1.51 1.79 Ituran 945 - - - - 25% 0.92 0.92 1.09 25th

percentile 14% 1.04 1.01 Median 21% 1.16 1.11 Mean 21% 1.40 1.18 75th percentile 28% 1.64 1.31 Kona $97 9 $3019 $27510 86%10 592%10 25% 0.12 n.m.11 n.m.11 Cost of equity 21 Weighted average cost of capital

(WACC) Sources: Company filings, Bloomberg, FactSet (as of February 25, 2026), Kroll Cost of Capital Guide, U.S. Federal Reserve, Management Notes: Informed by the range of the peer references as well as capital markets outlook Based on

current yield on 20-year U.S. Treasury (as of February 25, 2026) Based on the average of Kroll’s Supply-side ERP methodology (6.3%) and Historical ERP methodology (7.4%) per Kroll’s Cost of Capital Guide (as of December 31, 2025) Based on

size premia analysis per Kroll’s Cost of Capital Guide (average of 9th and 10th decile, as of December 31, 2025) based on target capital structure of 20% gross debt / capital, respectively Based on 600bps on latest 3-month SOFR (as of

February 25, 2026) 25% tax rate per Management Debt / capital and debt / equity interquartile range and mean exclude Ituran Based on peer mean 2-year adjusted historical beta (weekly periodicity, regressed against S&P 500) per Bloomberg

(as of February 25, 2026) Kona share price as of February 25, 2026; balance sheet as of December 31, 2025, per Management; FDSO includes 17.6m common shares and 1.5m RSUs as of February 25, 2026, per Management Illustratively includes

preferred stock as debt-like item. Preferred equity redeemed at 1.8x minimum return inclusive of accumulated PIK interest and value of 2.4m warrants issued to Samoa following November 15, 2025, per Management Not meaningful as R-squared is

0.001 Implied WACC Gross debt / capital1 Gross debt / equity Pre-tax cost of

debt 1.00 1.18 1.30 1.00 1.18 1.30 1.00 1.18 1.30 10.0% 11.1% 9.7% 1.08 1.27 1.41 15.1% 16.4% 17.3% 14.3% 15.5% 16.3% 15.0% 17.6% 9.7% 1.13 1.33 1.47 15.4% 16.8% 17.7% 14.2% 15.3% 16.2% 20.0% 25.0% 9.7% 1.19 1.40 1.54 15.8% 17.2% 18.2% 14.1% 15.2% 16.0% 25.0% 33.3% 9.7% 1.25 1.47 1.63 16.2% 17.7% 18.8% 14.0% 15.1% 15.9% 30.0% 42.9% 9.7% 1.32 1.55 1.72 16.7% 18.3% 19.4% 13.9% 15.0% 15.8% Risk-free

rate 2 4.6% Levered beta 1.40 Equity risk premium3 6.8% Size premium4 3.0% Size premium 17.2% Cost of debt Cost of debt (pre-tax) 5 9.7% A Appendix – Valuation supplement

STRICTLY CONFIDENTIAL STRICTLY CONFIDENTIAL 20% 32% 44% 53% 94% 25th

percentile Median Mean 75th percentile 90th percentile 22% 36% 42% 56% 81% 25th percentile Median Mean 75th percentile 90th percentile Premia paid analysis Share price premium 30-day1 Source: Refinitiv Notes: Analysis includes

172 take-private transactions since 2017 with EV values greater than $250m, excludes target businesses in financial services, real estate, energy, biotechnology and pharmaceutical sectors Unaffected date as of December 18, 2024, the day prior

to Samoa’s 13D filing Share price as of November 3, 2025, the day prior to the public announcement of the initial Samoa Group offer 22 A Appendix – Valuation supplement $2.84 $2.61 $3.05 $3.83 $2.40 $2.57 30-day prior to initial Samoa

Group offer3: $3.09 $3.71 $3.40 $3.94 $5.00 Implied Kona share price based on: $1.97 30-day prior to unaffected2: $1.40 $1.68 $1.54 $1.80 $2.27 $4.78 $5.74 $5.27 $6.11 $7.74 Implied Kona share price based on: $1.17 unaffected

price2: $3.98 close prior to initial Samoa Group offer3: Share price premium 1-day1

STRICTLY CONFIDENTIAL STRICTLY CONFIDENTIAL $ /

share Oct-21 Jul-22 Feb-24 Feb-25 Feb-26 Average target price $87.50 $50.50 $12.50 $7.25 $5.00 % Premium

2 118.8% 271.3% 129.4% 197.7% (1.8%) – $20.00 $40.00 $60.00 - 20% 40% 60% 80% 100% Oct-21 Aug-22 Dec-25 Buy Hold Jun-23 Apr-24 Feb-25 Sell Share price Target price $5.00 $5.00 $12.00 $2.50 $3.00 $1.50 Discontinued

coverage Analyst price targets Analyst sentiment since 2021 de-SPAC1 Analyst price targets 1 2 Number of broker recommendations 4 4 2 Average target price over time1 Sources: FactSet (as of February 25, 2026), Wall Street

research Notes: Target prices based on 100-day consensus window adjusted for 1:5 reverse stock split % Premium based on date of the median broker consensus price at the time 3. Unaffected date as of December 18, 2024, the day prior to

Samoa’s amended 13D filing Price target as of 11/13/25 Price target as of 11/13/25 Final coverage 12/13/24 Final coverage 08/15/24 Current price target Price target as of unaffected date3 Price target as of final coverage 23 A Appendix

– Valuation supplement Feb-26